Share Purchase vs Asset Purchase in Indonesia: Which One Should Investors Choose?

Key takeaways: A share purchase allows the investor to acquire the target company as a whole, including its assets, licences, contracts, employees, goodwill, and historical liabilities. An asset purchase gives the investor more flexibility to acquire only selected assets, but may require contract novations, licence reapplications, employee transition planning, and additional transfer steps. The right structure depends on the investor’s commercial objective, liability appetite, licensing needs, tax position, operational continuity, and long-term exit strategy. In Indonesia, acquisition structure should be decided early because it directly shapes due diligence scope, transaction documents, closing timeline, and post-closing risk.

Choosing the Right Structure: Five Questions Every Investor Should Ask

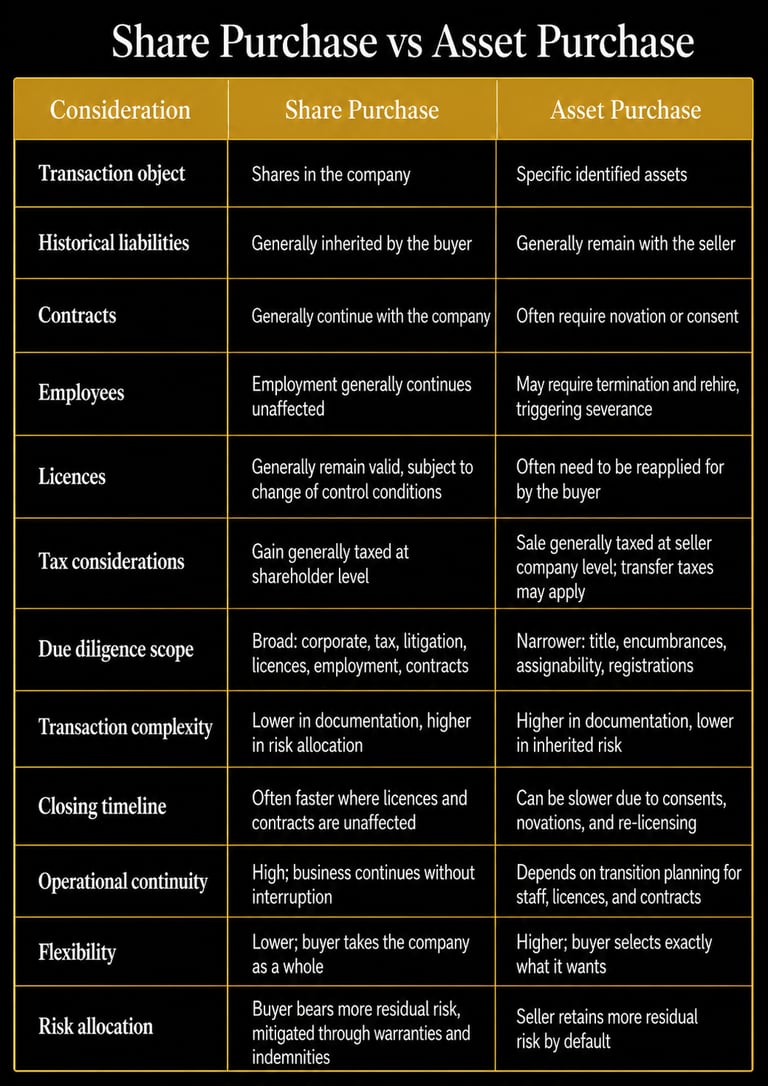

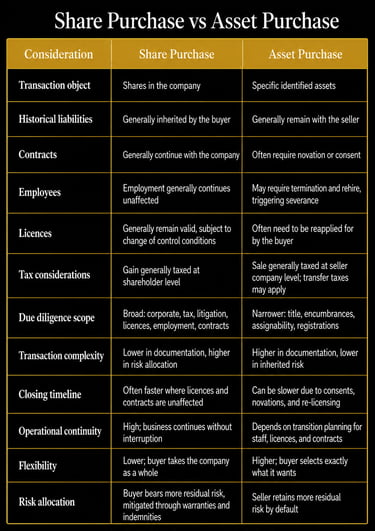

What exactly are you trying to acquire? A business relationship built on licences, brand, and customer goodwill points toward a share purchase. A specific set of assets or a single business line points toward an asset purchase.

Are you prepared to inherit historical liabilities? If the target has a complicated tax, litigation, or compliance history, that answer alone often decides the structure.

Will the business need to continue operating immediately after closing? Continuity of licences, contracts, and staff is generally far more straightforward in a share purchase.

Will licences or contracts require third party approval? If key counterparties or regulators need to consent to a transfer, that consent process should be mapped and timed before the structure is finalised, not discovered afterward.

What is your long-term investment and exit strategy? How the business is acquired often shapes how it can later be sold, financed, or restructured, so the exit should be considered as early as the entry.

Conclusion

There is no universally superior acquisition structure in Indonesia. The right choice depends on the investor's commercial goals, the legal and regulatory risks specific to the target, the tax efficiency of each option, and what the investor is ultimately trying to achieve, both at closing and years later at exit.

Getting this decision right at the outset shapes the entire transaction that follows, from the scope of due diligence to the shape of the closing documents. Before committing to a structure, it is worth having experienced Indonesian M&A counsel assess the target and the investor's objectives together.

Lexeron Advocates regularly advises foreign investors, private equity funds, and corporate acquirers on structuring, due diligence, and execution of share and asset acquisitions across Indonesia. If you are evaluating an acquisition and are unsure which structure fits your objectives, we welcome the opportunity to discuss it with you.

Almost every acquisition in Indonesia begins with the same fundamental question. Should the investor buy the target company's shares, or only the assets it wants to use? The answer shapes everything that follows: which liabilities the buyer inherits, which contracts and licences survive, how employees are treated, how the deal is taxed, and how long closing takes.

There is no universally better structure. The right choice depends on the investor's commercial objectives, the legal and regulatory risks attached to the target, the tax consequences on both sides of the table, how important operational continuity is on day one, and the investor's long term exit strategy.

This article sets out how share purchases and asset purchases work in Indonesia, where each structure tends to make commercial sense, and the practical questions investors should be asking before a term sheet is signed.

Understanding the Two Acquisition Structures

A share purchase involves buying the shares of the target company directly, either from its existing shareholders or through a subscription for new shares. The company itself does not change. It continues to exist, hold its own assets, employ its own staff, and operate under its own contracts and licences. What changes is who sits behind it as the shareholder. Under Law No. 40 of 2007 on Limited Liability Companies, as amended by Law No. 6 of 2023 (Undang-Undang No. 40 Tahun 2007 tentang Perseroan Terbatas or “UUPT”), a share transfer is generally a matter of updating the company's shareholder register and, for certain transactions, notifying the Ministry of Law. The company's obligations, both known and unknown, travel with it.

An asset purchase involves buying specific assets identified by the buyer, such as equipment, inventory, intellectual property, real estate, telecommunication towers, or selected contracts, rather than the corporate vehicle that currently holds them. The seller's company continues to exist and remains responsible for its own liabilities unless the buyer expressly agrees to assume particular obligations. Contracts the buyer wants to keep generally need to be novated or reassigned with the counterparty's consent, and certain licences may need to be reapplied for in the buyer's name depending on the sector and the terms of the original licence.

The distinction sounds technical, but its commercial effect is significant. A share purchase buys the whole box, including everything inside it that has not yet been discovered. An asset purchase lets the buyer choose only the contents it wants.

What Does the Investor Actually Acquire?

In a share purchase, the investor acquires the company as a whole: its assets, its liabilities, its employees, its licences, its existing contracts, its goodwill, and its complete history, including obligations that predate the acquisition and have not yet surfaced. In an asset purchase, the investor acquires only what is specifically listed in the transaction documents, typically selected assets, selected contracts, selected intellectual property, selected inventory, and selected equipment. Nothing transfers by default.

This difference is the single biggest driver of transaction risk. Consider an investor acquiring a manufacturing business with a strong customer base but a history of informal tax reporting. Buying the shares means buying that tax history along with the customers. Buying only the production assets and key supply contracts, and leaving the existing corporate entity and its tax history with the seller, isolates the buyer from that exposure, though it may also mean losing supplier relationships or permits that are tied to the seller's company rather than to the assets themselves.

Legal Risk Comparison

Share purchases carry a broader and less visible risk profile. The buyer steps into hidden liabilities that existed before closing, including pending or threatened litigation, historical tax exposure, employment claims, environmental non-compliance, and breaches of existing contracts that have not yet been raised by the counterparty. Warranties, indemnities, and price adjustment mechanisms in the sale and purchase agreement are the primary tools used to manage this risk, but they do not eliminate it. They only allocate who bears the cost if something goes wrong.

Asset purchases generally offer a cleaner risk profile, since the buyer is not automatically inheriting the seller's corporate history. The risks shift instead to execution: confirming the seller actually owns and can transfer each asset free of encumbrances, correctly assigning contracts that require counterparty consent, and completing any registrations needed to perfect the buyer's title, for example re-registering real estate, vehicles, or intellectual property in the buyer's name.

A realistic scenario illustrates why this matters. An investor negotiates to buy the shares of a well-known retail brand, attracted by its store network and customer loyalty. During due diligence, it emerges that several store leases contain change of control clauses giving the landlord a right to terminate on a change of shareholder, and that the company is defending an unresolved labour dispute from a prior restructuring. None of this would have transferred to the buyer in an asset deal structured around the stores and the brand alone, but in a share deal it comes with the company.

Regulatory and Licensing Considerations

Legal ownership of a business does not automatically guarantee uninterrupted regulatory compliance. Most operating businesses in Indonesia hold licences through the Online Single Submission (OSS) system, anchored by a Business Identification Number (Nomor Induk Berusaha or “NIB”), together with sector specific approvals depending on the business classification (Klasifikasi Baku Lapangan Usaha Indonesia or “KBLI”). Since June 2025, this framework has been governed by Government Regulation No. 28 of 2025 on Risk Based Business Licensing (“GR 28/2025”), which replaced the earlier 2021 licensing regulations and now serves as the primary basis for how these licences are issued, monitored, and transferred.

In a share purchase, the company's existing NIB and sector licences generally remain valid because the licence holder, the company itself, has not changed, though some licences carry conditions requiring notification or approval of a change in ultimate shareholding, particularly in regulated sectors such as financial services, mining, or telecommunications. In an asset purchase, licences attached to the seller's company typically do not transfer automatically with the assets, and the buyer will often need to apply for its own licences before it can lawfully operate the acquired business.

This is where deals are sometimes structured incorrectly. An investor buying only the production line and brand of a food manufacturer may assume it can begin operating immediately, only to discover that the health and safety certification, import licences, and halal certification were issued to the seller's company and do not automatically follow the machinery. Confirming which approvals are asset linked and which are entity linked should happen well before signing, not after the assets have already changed hands.

Employment Considerations

In a share purchase, employment relationships generally continue undisturbed, since the employer remains the same legal entity throughout. Employees are not required to consent to the transaction, and existing employment terms, tenure, and benefits carry over automatically.

An asset purchase raises a different set of questions. Because the buyer is often a separate legal entity from the seller, employees do not automatically transfer with the assets. Depending on how the deal is structured, this may involve terminating employees at the seller level and offering new employment with the buyer, which triggers statutory severance and other termination entitlements under Law No. 13 of 2003 on Manpower, as amended by Law No. 6 of 2023 (Undang-Undang No. 13 Tahun 2003 tentang Ketenagakerjaan or (“Manpower Law”), and its implementing regulation, Government Regulation No. 35 of 2021. Employee consent to the new arrangement is generally required, and the cost of statutory severance can be a material, and sometimes underestimated, line item in an asset deal budget.

An investor acquiring only the assets of a services business with a long tenured workforce should model the severance cost of the transition carefully. In some cases, the economics of retaining staff through a share deal, inheriting their tenure but avoiding a termination bill, compare more favourably than an asset deal that looks cleaner on paper but triggers significant one-time employment costs.

Tax Considerations

Tax treatment differs meaningfully between the two structures and should be analysed early, not treated as a closing formality. Broadly, a share purchase is typically a transaction between the buyer and the selling shareholders, with income tax implications for the sellers on any gain, while the target company's own tax position, including any historical exposure, remains with the company after closing. An asset purchase is generally treated as a sale of specific assets by the seller company, which can trigger income tax and, depending on the nature of the assets, value added tax at the level of the seller, while the buyer separately needs to consider transfer related taxes on items such as real estate. Indonesia's tax framework in this area continues to be shaped by Law No. 7 of 2021 on the Harmonisation of Tax Regulations.

This is not intended as tax advice, and every transaction should be reviewed by qualified tax counsel before the structure is finalised. What experienced dealmakers do consistently is model the tax consequences of both structures early in the process, since the tax outcome can materially affect purchase price negotiations and sometimes changes which structure makes commercial sense in the first place.

An investor comparing a share deal against an asset deal for the same target may find that the headline price looks similar, but the after-tax proceeds to the seller, and the deductible cost basis available to the buyer going forward, differ enough to shift the seller's preference strongly toward one structure over the other. That preference is a negotiating factor in its own right.

Legal Due Diligence: Why the Scope Changes

Due diligence is not a fixed checklist. Its scope is dictated by the structure chosen, and in a well-run transaction, due diligence findings often influence which structure ultimately makes sense, rather than simply confirming a decision already made.

For a share purchase, due diligence needs to cover the target company comprehensively: its corporate history and governance, any pending or historical litigation, its full tax position, all licences and regulatory approvals, employment arrangements across the workforce, the complete contract portfolio, general compliance, and intellectual property ownership. Because the buyer inherits the company as it stands, gaps in this review become the buyer's problem after closing.

For an asset purchase, due diligence narrows to the specific assets being acquired: confirming the seller's ownership and title, checking for encumbrances such as liens or mortgages, assessing whether key contracts can actually be assigned or require third party consent, and identifying which registrations need to be updated to perfect the buyer's ownership. The scope is narrower, but precision matters more, since anything left off the asset list simply does not transfer.

When Is a Share Purchase More Suitable?

A share purchase tends to make sense when the investor wants to acquire an operating business as a going concern: when preserving existing licences matters, when customer relationships and contracts are tied closely to the corporate entity, when an established brand and its accumulated goodwill are central to the deal's value, and when business continuity from day one is a priority.

A private equity fund acquiring a regional hospital operator, for example, is unlikely to want to disturb the network of medical licences, insurance panel agreements, and accreditation built up over many years. A share purchase preserves all of that in place, provided due diligence has properly surfaced the risks that come along with it.

When Is an Asset Purchase More Suitable?

An asset purchase tends to make more sense for distressed businesses where historical liabilities are a serious concern, for selective acquisitions where the investor only wants one division or business line rather than the whole company, and for deals centred on discrete assets such as manufacturing equipment, real estate, or intellectual property rather than the ongoing business built around them.

A strategic investor interested only in a target's manufacturing line and its patent portfolio, but not its legacy retail division or its litigation history, is often better served by an asset purchase that isolates exactly what it wants and leaves the rest, including the risk, with the seller.

Comparison Table